How to

Search

Find

How to

Join

Play Video

Video time control bar

0:00

▶️

⏸️

🔊

Audio volume control bar

0:00

/

0:00

↘️ 0.25

↘️ 0.5

↘️ 0.75

➡️ 1

↗️ 1.25

↗️ 1.5

↗️ 1.75

↗️ 2

↔️

↕️

Timecodes:

Related videos:

Forward Rate Agreements Explained | How to Calculate an FRAs Value

Bond Duration and Bond Convexity Explained

Bootstrapping Spot Rates From the Par Curve

What is Yield to Maturity? | How to Calculate YTM? | CA Rachana Ranade

Spot Rates & Forward Rates | Exam FM | Financial Mathematics Lesson 30 - JK Math

How to Calculate Spot Rates, Forward Rates, and Discount Factors

CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr. Arif Irfanullah part 5

What is the Yield Curve, and Why is it Flattening?

Relationship between bond prices and interest rates | Finance & Capital Markets | Khan Academy

Forward rates are implied by zero rates (FRM T3-11)

Interest Rate Swaps Explained | Example Calculation

Bond Duration Explained Simply In 5 Minutes

The Term Structure of Interest Rates Spot, Par, and Forward Curves (2024 CFA® Level I Exam – FI 9)

Modified Duration

Confused between rates - Spot, Forward, Coupon, Current Yield, IRR, YTM, BEY

Spot Rate vs. Forward Rates (Calculations for CFA® and FRM® Exams)

What is a swap? - MoneyWeek Investment Tutorials

The Spot Curve and Forward Curve Explained In 5 Minutes

FRM: TI BA II+ to compute bond price given zero (spot) rate curve

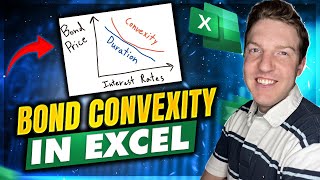

Calculate Bond Convexity and Duration in Excel | Interest Rate Risk