How to

Search

Find

How to

Join

How to sell shares of s corporation

sell

Sale of S Corporation Stock: Section 1.1368-1(g) Election

Play Video

Video time control bar

0:00

▶️

⏸️

🔊

Audio volume control bar

0:00

/

0:00

↘️ 0.25

↘️ 0.5

↘️ 0.75

➡️ 1

↗️ 1.25

↗️ 1.5

↗️ 1.75

↗️ 2

↔️

↕️

Timecodes:

No transcript (subtitles) available for this video...

Other suggestions:

What Is the Basis for My S-Corporation?

Understanding S Corp Distributions: A Simple Guide for Business Owners

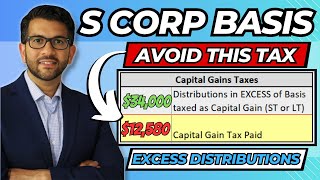

S Corp Basis Explanation | Distributions in EXCESS of Basis

The EASIEST Breakdown: LLC vs S-Corp for your trading business

How to Structure the SALE of a Business? | Stock Sale vs Asset Sale

What is a shareholder basis?

✅ S Corporation Taxes Explained in 4 Minutes

Understanding 2024 Capital Gains Tax Changes in Canada

How to Sell or Transfer LLC Membership Interest to a Person, Trust or Company

Issuing Stock

Asset vs. Share Purchase | How to Sell a Business, How to Buy a Business - David C. Barnett

S-Corp explained in under 4 minutes

Taxes on Stocks Explained for Beginners that Know NOTHING About Taxes

How Many Shares Should I List for my LLC or Corporation?

IRS Form 7203 - Sale of S Corporation Stock with Suspended Losses

DO NOT Open an S-Corp in 2023!

How to Handle Taxes After Selling Your Business

IRS Form 7203 - S Corporation Loss Limitations on Stock Basis