How to

Search

Find

How to

Join

How to sell real estate in colorado

sell

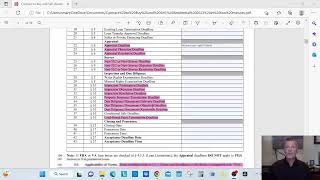

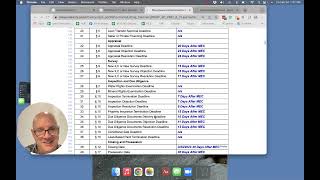

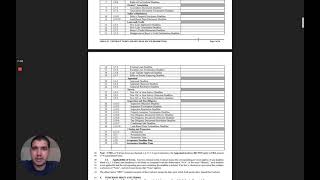

Understanding the Colorado Contract to Buy and Sell Real Estate for Homebuyers

Play Video

Video time control bar

0:00

▶️

⏸️

🔊

Audio volume control bar

0:00

/

0:00

↘️ 0.25

↘️ 0.5

↘️ 0.75

➡️ 1

↗️ 1.25

↗️ 1.5

↗️ 1.75

↗️ 2

↔️

↕️

Timecodes:

No transcript (subtitles) available for this video...

Other suggestions:

Colorado Contract to Buy and Sell Real Estate in Five Minutes

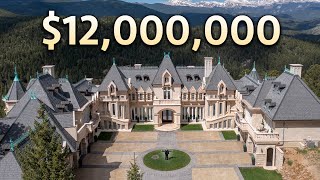

Inside a $12,000,000 Newly Built Colorado Modern Castle with Mountain Views!

2023 Colorado Contract to Buy Sell Real Estate

40 Acres of Colorado Land for Sale in Rocky Mountains • LANDiO

This $21,000,000 Luxury Colorado Ranch Offers the Very Finest in Natural Setting

The Alarming Reasons Everyone is Leaving Colorado

How to Sell Your Home Fast in the Competitive Colorado Real Estate Market

How to Sell Real Estate in a Colorado Divorce and Privacy

Colorado Contract to Buy and Sell Real Estate - Residential with Peter Psotny

New Agent Training Colorado Contract To Buy And Sell Real Estate Purchase Agreement

State lawmakers consider proposal to lower property taxes in Colorado

CONTRACT TO BUY and Sell Real Estate-Denver, COLORADO

What is a Short Sale? - How Do Short Sales Work?

Colorado Home Purchase Contract 2023 | Contract to Buy and Sell Real Estate

The Best Time To Sell Real Estate In Boulder Colorado

Why You Don’t Want To Buy Vacant Land

How Do I Sell My House Without An Agent In Colorado #realestate

How to Start Flipping Houses as a Beginner