How to

Search

Find

How to

Join

How to sell premium financing

sell

Premium Financing Explained for Wealth Managers and Insurance Agents

Play Video

Video time control bar

0:00

▶️

⏸️

🔊

Audio volume control bar

0:00

/

0:00

↘️ 0.25

↘️ 0.5

↘️ 0.75

➡️ 1

↗️ 1.25

↗️ 1.5

↗️ 1.75

↗️ 2

↔️

↕️

Timecodes:

No transcript (subtitles) available for this video...

Other suggestions:

How Premium Finance Works

Life Insurance Sales - Selling Premium Finance

Buy-Sell Agreements with Premium Financing

What is Premium Finance for Life Insurance?

Premium Finance Life Insurance For Your Clients | Selling Life and Annuities

Premium Finance Gone Wrong - PLEASE avoid this design

Premium Financing - What Is It & Why Should You Care

Magnificent Seven Earnings in the Spotlight | Bloomberg Businessweek

Premium Financing: How It Works

What you and your clients need to know about Premium Financing

Premium Finance dos and donts - Part 1

How to Start an Insurance Premium Financing Company

The Architecture Of A Premium Financing Sale

Premium Financing Life Insurance

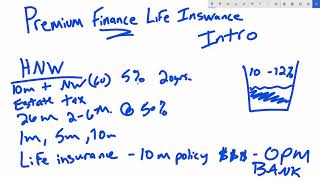

Premium Finance Life Insurance - Series Intro

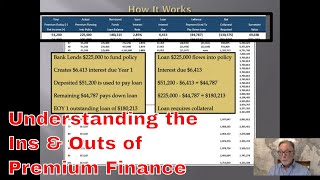

The Ins and Outs of Premium Finance

Premium Financing Done the Right Way

Premium Finance - Too good to be true - Using Indexed Universal Life