How to

Search

Find

How to

Join

How to sell preferred stock

sell

Profiting from the Pivot: Preferred Stocks

Play Video

Video time control bar

0:00

▶️

⏸️

🔊

Audio volume control bar

0:00

/

0:00

↘️ 0.25

↘️ 0.5

↘️ 0.75

➡️ 1

↗️ 1.25

↗️ 1.5

↗️ 1.75

↗️ 2

↔️

↕️

Timecodes:

No transcript (subtitles) available for this video...

Other suggestions:

What is a Preferred Stock - Preferred Stocks 2018

Why I Prefer to Avoid Preferred Shares | Common Sense Investing

23. Calculate Yield to Call and How to buy Preferred Stock

A look at investing in preferred stocks versus common stock

Liquidation Preferences and Participating Preferred Stock: How VC Terms Affect Deals

22. What is Preferred Stock

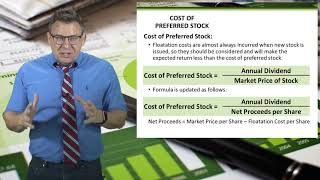

Cost of Preferred Stock

Nifty 22,350 a key resistance level; BFSI stocks in focus

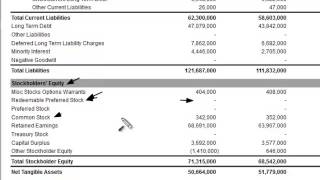

Redeemable Preferred Stock on the Balance Sheet

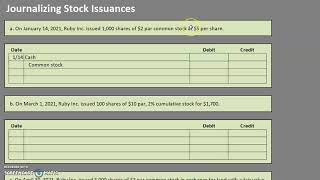

Journalizing the Issuance of Stock (Common Stock, Preferred Stock, Cash and Land)

What is a Preferred Share?

High Dividends AND Lower Taxes - These Investments Are Often Overlooked

Convertible Preferred Stock Explained.

Common Stock vs Preferred Stock | Top Differences You Must Know!

Convertible Preferred Stock. CPA Exam

Convertible Preferred Stock Explained

Diversify Your Dividend Stock Portfolio with Preferred Stock ETF's!

Winans Preferred Stock Studies